If you’re paying any attention to the housing market lately, you’ve probably noticed that mortgage rates are hitting record highs, that we haven’t seen the likes of for more than 15-years. And, if you’re like millions of Americans considering buying a house right now, you are probably wondering what all of this means for your future home-buying plans. Well, we’re here to offer some guidance and bring some good news. Whether you own your house and are thinking about moving, or rent and want to become a first-time homeowner, it could still be a good option for you to buy a home and will most likely work out in your favor over the long term.

Higher Interest Rates = Lower Home Prices

As the market has demonstrated over and over again, rising interest rates will inevitably be accompanied by falling home prices. Just in the past few months, data from RedFin shows the median sale price of a home for sale in Wenatchee has plummeted by nearly 25% over the past 3 months since peaking in June 2022. Homes are still selling for slightly above the median price of a year ago, but they are not expected to keep rising as before. As local realtor Danny Zavala points out in this article on the Wenatchee area housing market in Wenatchee, “It’s still very active. There’s still a lot of buying. There’s still a lot of listings. But we’re starting to see a more healthy real estate market.”

Marry The Mortgage, Date The Rate

Lenders and realtors have a saying to “marry the mortgage and date the rate” — it’s an archaic way of recommending to secure the lower home price that this high interest market is creating, then plan to renegotiate your interest rate at a future time by refinancing when interest rates are more favorable again. Although it may seem risky at first glance, history has shown that home values will continue to increase overtime; meanwhile interest rates will fluctuate based on the ebbs and flows of the market.

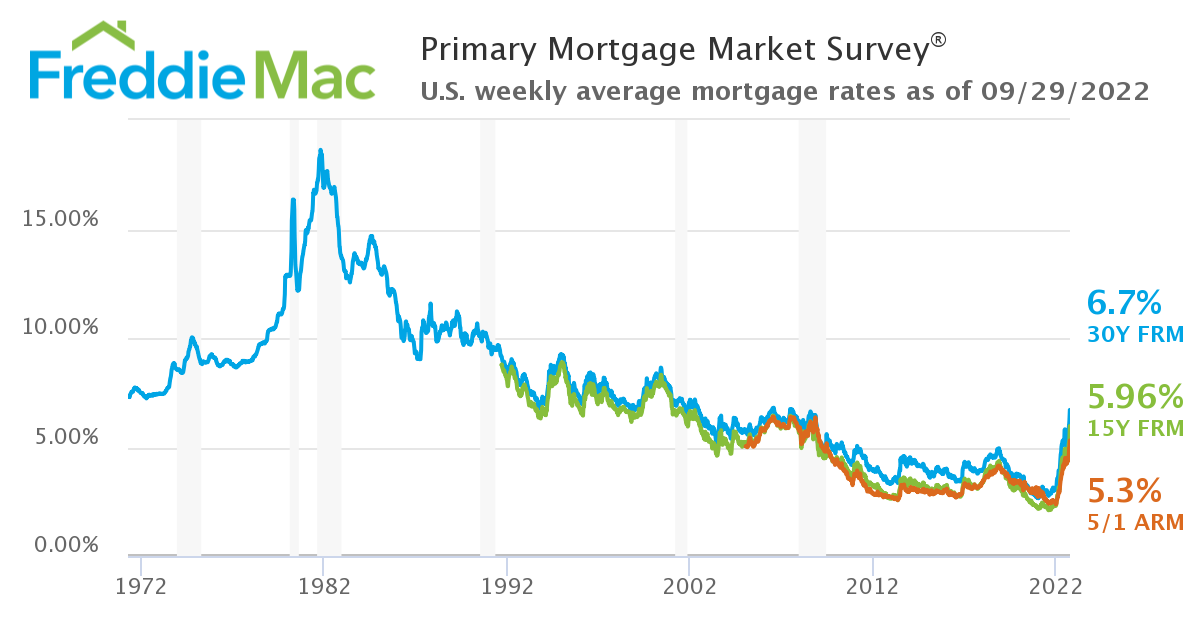

So, even though interest rates seem astronomically high at the moment, especially when compared with the rates of just a few months ago, they are still relatively low when we zoom out and look at the bigger picture. In 1990 the average mortgage rate was up to 10.31%. This rate steadily declined over the following 2 decades down to 5.14% in 2010, then continuing to fall steadily over the next decade with some small ups and downs along the way, leading us to where we are now in the present day market.

Understand Your Loan Options

When it comes to the lending for buying a home, there are many different ways to structure your loan. As Freddie Mac points out on their website, the type of loan that you choose will ultimately affect the monthly payment and overall cost of your loan, making it a hugely important decision for your future financial well-being.

Whether you choose a fixed-rate or adjustable rate mortgage (ARM), what’s most important is to consider is what makes sense for you and where you’re at right now. How much money do you have for a down payment? What is your monthly budget to pay back loan? How long do you plan to own your home for? What is your risk factor? These are all questions highly worth considering when making your decision. We recommend you also do your own research and schedule to meet with a mortgage lender (or 2, or 3!) to further discuss what your best options are.

Renting Is Expensive

If you’re currently renting, then you don’t need us to tell you how expensive it is to rent right now (not to mention hard to find!). Just like the rise in home prices over the last 2 years, rent prices have also rapidly gone up. This Zillow report demonstrates how in just the last year, the average cost to rent in Wenatchee went up $600 per month, from $1600 to $2200/month on average! And, unlike the predictions of falling home prices, rental rates are expected to remain steady, or even increase, due to limited vacancy combined with the nature of signing a lease months in advance and locking in your rate for 12-24 months.

If you are currently having a hard time keeping up with rent, then it’s unlikely you are prepared to buy a home at this time. However, if buying a home was something you were already considering and you have been taking the next steps to make that happen, meet with a professional to get a realistic idea of what your monthly payments would be. You might be surprised to find out that your mortgage payments are just as much as you’re paying for rent, or possibly less. And even if those payments are slightly more than what you’re paying now renting, consider that this money is going back into your pocket and not someone else’s.

Homeowners Are More Wealthy

As this article by Forbe’s points out, “Homeowners have a net worth that is more than 40 times greater than their renter counterparts.” This shocking static came from a Survey of Consumer Finances carried out by the Federal Reserve in 2020, showing that, “Homeowners had a median net worth of $255,000 in 2019; renters had a median net worth of just $6,300.” Of course, it’s not as simple as just buying a home and watching your wealth soar, but it could be a smart step toward your financial success, especially if you’ve already started taking steps in that direction.

The Takeaway

It’s hard to know what the next 5, 10, 20 years of the housing market will have in store, but we do know that there are many benefits to owning a home. Besides the satisfaction that comes with making a house your home, it also brings opportunities to grow your wealth and invest in your future. Renting is also very expensive, so if you can afford to move out you can at least put your money toward your own assets. And finally, although interest rates are an important factor when buying a home, they are only one of many factors and should definitely NOT be the only thing you base your decision on.